While the earlier analysis focused on what could change, this article takes the next step—offering a deeper look at how proposed CGT and negative gearing changes may reshape investment structures, cashflow, and long-term strategy.

___

The 2026 Federal Budget has introduced major reforms to negative gearing and Capital Gains Tax (CGT), changing how investors approach tax planning, cashflow management, portfolio structuring, and long-term strategy.

Naturally, many investors are now asking:

- Should I only buy new builds?

- Are established properties still worth investing in?

- Should I move investments into an SMSF or company?

- Will these changes reduce the long-term benefits of property investing?

The reality is far more nuanced than the headlines suggest.

The reforms do not eliminate the advantages of property investing. Instead, they change when tax benefits are received, which structures become more attractive, and how investors need to think strategically moving forward.

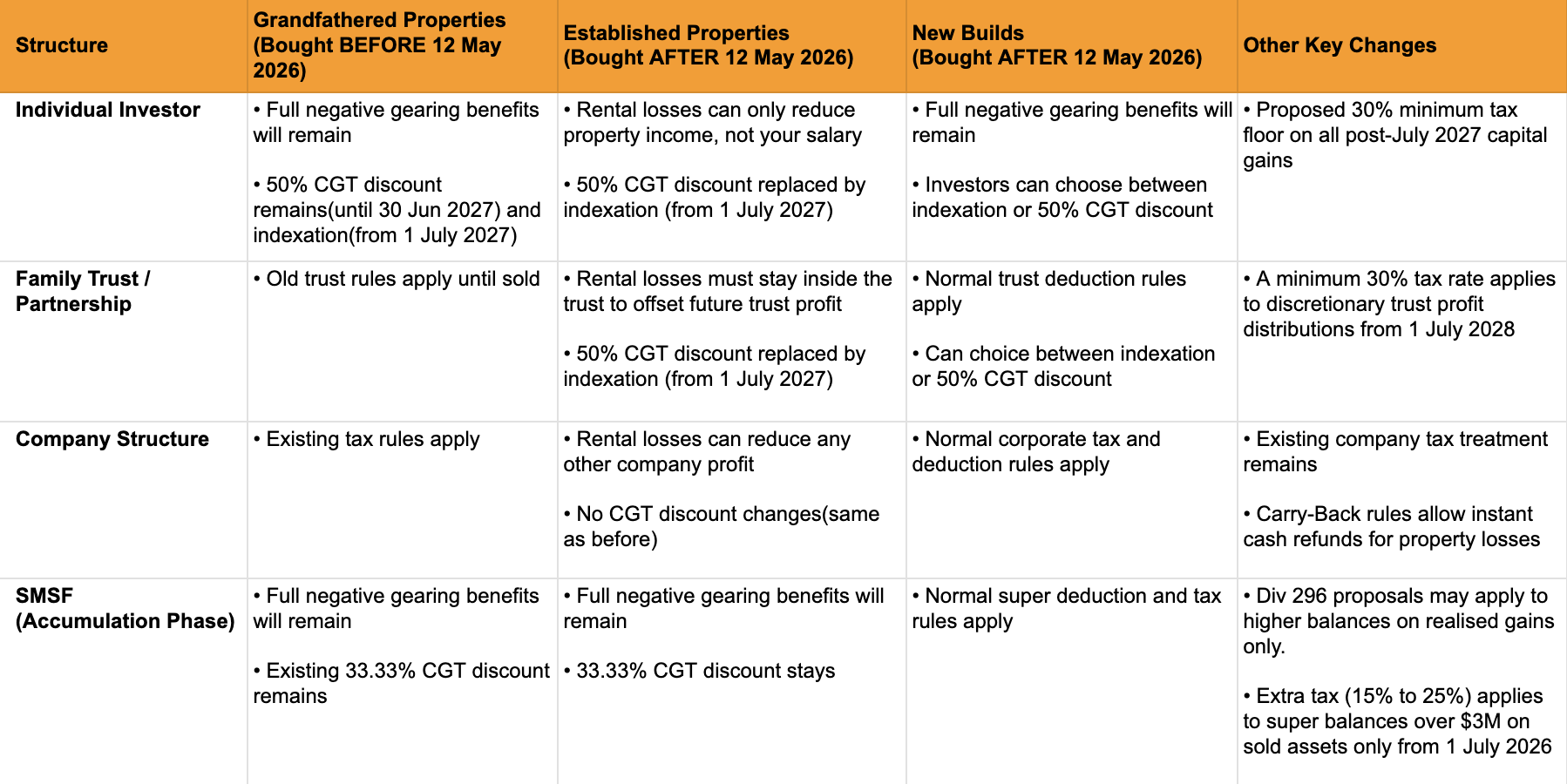

New Policy Changes (Purchased Post-12 May 2026)

*Trust distribution tax floor begins 1 July 2028.

Summary of "New" vs "Grandfathered"

- Grandfathering: If you bought before 7:30pm yesterday, none of the "NEW" labels above apply to you. You keep your current benefits for the life of that asset.

- The "New" Target: The government has specifically targeted Individuals and Trusts to reduce their tax advantage on existing houses, while leaving SMSFs and Companies largely as they were to encourage professional and long-term investment.

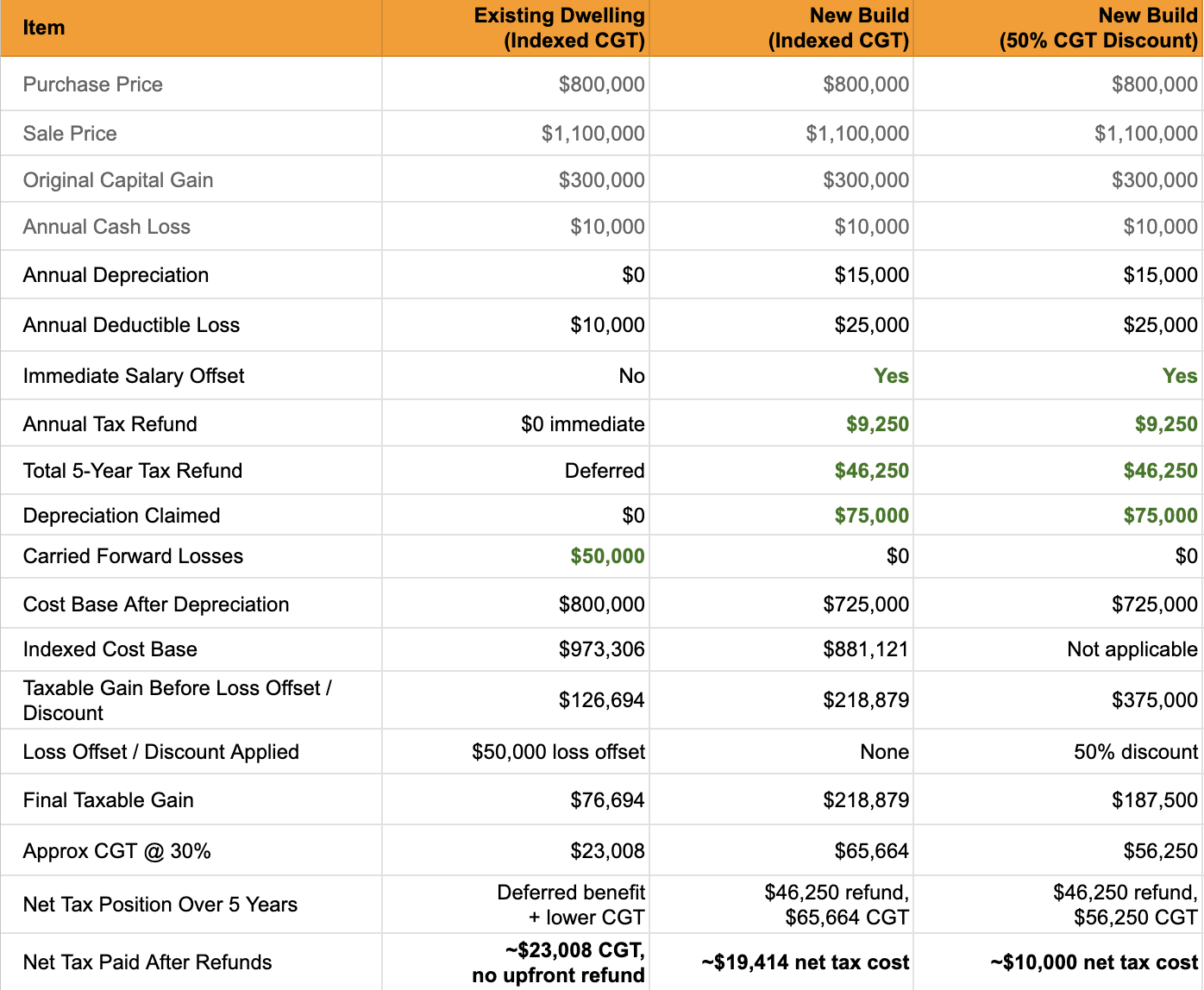

Example Cashflow Comparison

To better understand the practical impact of the reforms, let’s compare a simplified investment scenario across three different property strategies.

Assumptions

- Purchase Price: $800,000

- Sale Price After 5 Years: $1,100,000

- Total Capital Growth: $300,000

- Inflation / Indexation: 4% annually

- Annual Cashflow Loss: $10,000

- New Build Depreciation: $15,000 annually

Side-by-Side Property Strategy Comparison

As the comparison shows, the overall differences between these scenarios are not as dramatic as many investors may initially assume. In many cases, making the wrong investment choice, selecting the wrong market, or chasing short-term tax benefits without strong fundamentals could have a far greater impact on long-term performance than the tax structure itself.

What Investors Should Focus on Moving Forward

1. Don’t Buy Solely for Tax Benefits: While the reforms create stronger incentives toward new builds, tax benefits alone should never drive the entire investment decision.

Construction costs across Australia have increased significantly in recent years, and not all new developments will deliver strong long-term performance. Investors still need to carefully assess location quality, supply levels, owner-occupier demand, infrastructure growth, and long-term market fundamentals before making a decision.

A poor-quality property with strong tax benefits can still produce poor long-term results.

2. Strong New Builds May Benefit Long Term: New builds located in areas supported by strong infrastructure investment, population growth, employment expansion, lifestyle appeal, and genuine housing demand may continue performing strongly over the long term.

In these markets, the combination of depreciation benefits, stronger cashflow support, ongoing negative gearing incentives, and long-term demand may create attractive long-term investment outcomes.

3. Established Properties May Benefit Differently: Established properties may also strengthen under the new framework, particularly in tightly held suburbs with strong owner-occupier demand and limited future supply.

As more investors hold onto grandfathered properties for longer periods, supply in certain established markets could tighten further, potentially placing upward pressure on both property prices and rental values over time.

4. Rental Shortages Could Push Rents Higher: In locations already experiencing housing shortages and low vacancy rates, rental pressure may continue increasing if supply cannot keep pace with population growth and demand.

This could improve long-term cashflow outcomes for well-selected investment-grade properties located in supply-constrained markets.

5. Scarcity and Land Value May Matter More: As speculative demand weakens, quality assets may stand out more clearly.

Properties supported by strong underlying land value, limited future supply, and genuine owner-occupier appeal are likely to maintain stronger long-term demand, potentially widening the gap between investment-grade assets and average properties over the next cycle.

6. Oversupply Risk Could Increase in Some Markets: Not all new developments will perform equally, particularly in locations where large volumes of similar stock continue entering the market.

Investors should be cautious about chasing tax incentives in oversupplied markets where weaker owner-occupier demand, elevated supply levels, or inflated pricing may limit long-term growth potential.

7. Cashflow Strength May Become More Important: The reforms may shift investor focus away from relying heavily on tax refunds to support underperforming properties.

Instead, greater emphasis may be placed on stronger rental demand, sustainable holding costs, low vacancy markets, and long-term cashflow resilience when assessing investment opportunities.

8. Diversification Could Become More Important: The next cycle is unlikely to produce uniform performance across all cities, suburbs, and asset types.

Some markets may benefit from affordability migration, infrastructure investment, and population growth, while others may struggle with supply pressure or weaker economic conditions. As a result, diversification across locations, asset types, and strategies may become increasingly important in managing both market and policy risk.

9. Structuring and Long-Term Planning Matter More Than Ever: As taxation rules evolve, ownership structuring and long-term planning may play a much larger role in investment outcomes.

Borrowing capacity, tax efficiency, succession planning, asset protection, and portfolio flexibility are no longer side considerations — they become central components of long-term investment strategy.

10. Long-Term Investing May Be Rewarded Again: The move toward inflation-indexed CGT may encourage a return to longer-term investing and more disciplined portfolio building.

Rather than short-term speculation, investors may increasingly focus on compounding growth, long-term wealth creation, and holding high-quality assets through multiple market cycles.

Final Takeaway

The proposed reforms do not make one property type or ownership structure inherently superior. What they do is shift the focus back to fundamentals.

As reliance on tax-driven outcomes reduces, long-term performance will increasingly be shaped by asset quality, market selection, cashflow resilience, and thoughtful structuring aligned with long-term goals. Investors who continue to chase incentives alone may struggle, while those who take a strategic, fundamentals-led approach are more likely to build resilient portfolios.

At InvestorPro, we help clients navigate this shift by focusing on investment-grade opportunities backed by strong fundamentals—scarcity, infrastructure growth, and genuine demand—while building portfolios that are diversified, well-structured, and positioned for long-term performance.

The next decade is unlikely to reward the fastest investors, but the most strategic.

Want to understand how these reforms may impact your investment strategy? Book a free discovery call to review your portfolio and position yourself strategically for the next phase of the market.